Beta and the rate sensitivities of deposits is a hot topic when talking about interest rate risk. Understanding your deposits and predicting their behavior and rate sensitivities (beta), along with anticipating how the credit union board and management may respond to changing interest rates is essential to estimating, monitoring, and managing interest rate risk. An important part of any interest rate risk program is knowing the beta, lag, and decay rate of the funding sources. This article will focus on the beta and lag trends for non-maturity deposits and how they are affecting net interest income.

Beta is defined as the deposit rate changes relative to market rate changes and is expressed as a percentage. For example, if deposit rates change 40 basis points while market rates change 100 basis points, it would equate to a beta of .40%. Betas can differ depending on the type of product, and the current level of rates, as well as the direction and magnitude of rate changes. Lag is the amount of time from a market rate change to when the credit union responds and increases rates. The response may be to preserve deposits or simply to give back to the members as income increases.

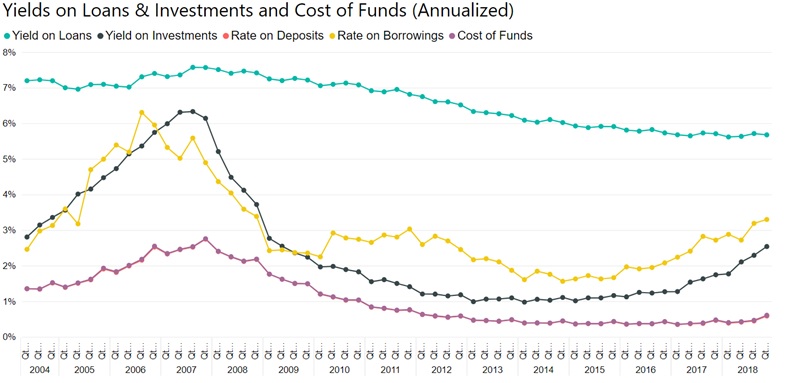

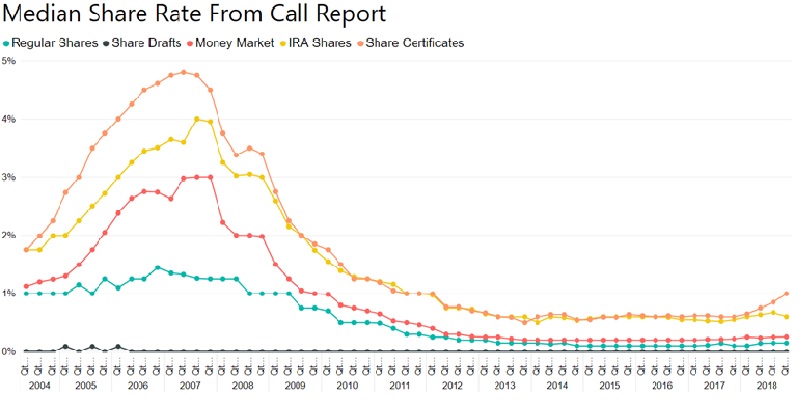

Stable and low beta funding, often referred to as core funding, is a large factor in mitigating the rate risk of holding long-term fixed rate assets. Non-maturity deposits have been studied and tracked, and it is accepted in the credit union industry that a large percentage of regular share and share draft deposits qualify as core funding. The cost of these deposits can be controlled as market rates increase. The data in the graph below supports the low rate sensitivities of regular shares and share drafts. The following two graphs show the yields on loan and investment along with the cost of funds, and the median share rates from an aggregate of call report data including December 2018.

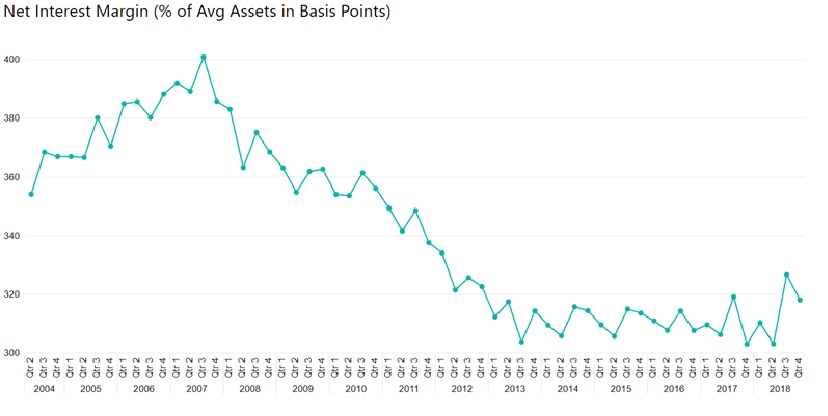

Now that the federal reserve has slowed down their rate hikes, we have seen investment yields pull back. It might be assumed that further increases in deposit rates would not be necessary. We know that regular shares have some rate sensitivity, but it remains very low. What is uncertain is how long the lag is going to remain before some rate increase occurs. Loan yields have not increased due to competitive pressures and may remain stagnant moving forward due to continued competition and economic conditions slowing down. Credit unions should not rule out the possibility that deposit costs will rise during the remainder of 2019, especially in CDs and money markets. The rate increases in these more rate-sensitive accounts may move more quickly than loan yields, and the expansion in the net interest margin that many credit unions have recently experienced may decline. Most of the improvement in the net interest margin has come from increased investment yields and minimal cost of fund changes. The trends indicate net interest margins improved as interest rates increased. The trend is contrary to many regulatory expectations, but consistent with historical trends and forecasted results of most ALMPro clients.

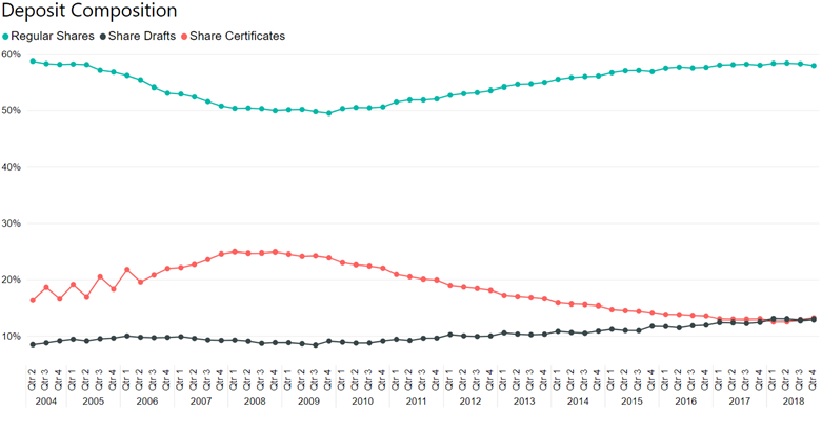

There has been talk that funds which may have been asleep since the great recession, or funds that came in as a flight to safety, may be waking up to higher rates available in the market, or members who have been sitting on the sidelines are starting to act. As I have talked with credit union management about the decline in CD balances, they say most of it remained in the credit union and is residing in regular shares. Many managers think the money is waiting to move back into CDs, but the big question is when. I have talked to other credit unions that have watched money leave for opportunities in the market place. Understanding your credit union trends is important. The Deposit Composition graph below indicates little movement thus far when looking at the total of all credit unions. If and when this shift begins for some credit unions or increases for others, the funding costs will rise, even if the credit union does not raise their rates further.

We are witnessing advertisements from other financial institutions with attractive rates for special savings accounts and CDs. These attractive rates are coming from both large and small financial institutions seeking to build their retail funding through CD specials. The liquidity that was in the marketplace after the recessions is diminishing. If you do not need to retain deposits, then you remain in control of your funding costs. On the other hand, if you are experiencing continued loan growth combined with stagnant or declining deposits, then pressure to increase deposit rates may not be avoidable.

Below is a graph of the recent rate and beta trends from a national perspective. Regions or even individual credit unions may be experiencing different trends. Being aware of the trends at your credit union, understanding your deposit structure, “caring about your beta,” and incorporating that information into your interest rate risk model are all essential when considering options that may include longer asset terms to increase earnings while monitoring and controlling your interest rate risk.