On December 11th, 2019, the Federal Reserve left short-term interest rates unchanged at a target range of 1.5% to 1.75%. This year, the Federal Open Market Committee cut rates three times but signaled it was unlikely to extend the easing cycle into 2020 unless there were material changes to the economy. The three rate cuts and the unease about the future economy lead to the question about negative interest rates which is on the minds of many board members and managers.

Emphasis is placed on increasing interest rates and the anticipated adverse effect on net interest margins and liquidity, and not much attention given to the implications of declining interest rates. When interest rates were at historic lows for such a long time, interest rate risk in the down-rate analysis was quickly glossed over and passed as unrealistic. In the same vane, NCUA’s list of supervisory priorities includes the potential negative effects of rising interest rates and very little is mentioned about declining interest rates.

During the past few years, as rates went up, deposit growth continued, funding mix did not significantly change, loan growth increased, and many investment portfolios completely repriced to the higher yields. Therefore, during this period of rising interest rates, many credit unions also experienced improved net interest margins and ROA. The improved earnings throughout the credit union system confirmed the results of the ALM models that forecasted improvement in net interest margins when interest rates increase. The improved net interest margins can be attributed to a significant portion of the credit unions’ loan and investment portfolio repricing in 3 years or less, and a large percentage of funding is stable with low rate sensitivities.

Now that interest rate trends are shifting and moving down, most credit unions need to prepare for a negative impact on earnings. As stated above, the interest rate risk scenarios in the up-rate typically forecast positive results, and interest rate risk lies in down rates. Also, many of the down-rate forecasts are showing results that exceed policy limits and boards and management are becoming more worried about down rates or even negative interest rates. When the down-rate scenarios are forecasting a decrease in net interest margins, the direction of the decline should be taken seriously. The amount of the drop should be further evaluated for reasonableness. If the forecasts are showing net interest income changes are outside policy guidelines, researching and understanding the details and assumption inputs becomes critical in determining if the results warrant attention and corrective action.

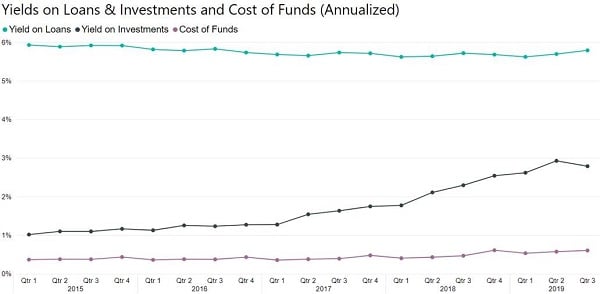

The graph above shows that loan rates lagged considerably and did not increase when market rates were increasing. We began to see small increases in the past two quarters and now interest rates are going back down. Investment yields improved and the cost of funds nudged up a bit. As short-term interest rates decrease, investment yields are directly correlated and will also decrease, but loan yields and the cost of funds may not change with the market. If a credit union holds a large investment portfolio, the interest income is going to be negatively impacted more than a credit union that has a smaller investment portfolio.

Interest rate risk management is a balancing act between risk and reward. If interest rates are moving down, investing and lending in long-term fixed-rate products lock in current yields and help future interest income. On the flip side, if a credit union makes mortgage loans or invests longer-term in preserving interest income now and then rates turn and start to go back up, the ability to increase interest income is limited. This conundrum, whether it be loans or investments, is best solved by sticking to a strategy and within well thought out interest rate risk limits, and not trying to guess or time the market.

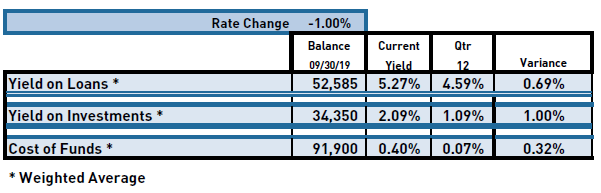

On the funding side of the balance sheet, costs are easier to manage and control in a down-rate scenario. However, since dividend rates did not go up much and remain low, the ability to reduce the cost of funds is severely restricted. The following example illustrates the change in yields and dividends in a down 100 basis points scenario. The credit union’s loan yields, based on repricing assumptions, are forecasted to move from 5.27% to 4.59%, and investments yields decline from 2.09% to 1.09% over 12 quarters. The cost of funds is at 0.40% and can only go down to 0.07%. The limitation and cause of most of the interest rate risk as rates go down is due to the inability to reduce the cost of funds below 0%. If deposit rates get to 0%, but loan yields and investment yields continue to decline, a solution would be to charge members for keeping their money safe and facilitating transactions. This is an example of negative interest rates. The likelihood that negative rates will become real for credit unions is very low. Large institutional investors and large financial institutions would implement negative rates before credit unions.

In this environment, the goal should be to preserve loan yields, move funds out of the investment portfolio into loans, and stick to your investment strategies. Lastly, reduce the cost of funds but understand the limitations we discussed above. Be mindful that fee income and other non-interest income are crucial components to maintaining ROA as rates go down.

A down-rate environment will unwind the improvements in net interest margins credit unions experienced in the last few years. The goal of this article is to caution, encourage preparedness, and inform that the down-rate scenarios in your ALM analysis should not be ignored. The assumption that loan rates will decline more than they went up when market rates increased by over 2% may indicate more interest rate risk in your analysis than may occur. Discussing and understanding the results of the down-rate forecasts is essential when comparing the results to policy limits. If the results are out of policy limits, determine if the results are realistic, and if corrective action is warranted. Lastly, document this process as part of the ALCO or board meetings.